And whenever expense increases for the company, the company debits the interest expense account and vice versa. In the above example, everything is similar to the previous examples that we have worked out. The only difference in this example is the period when the interest expense has to be paid. The reverse of interest payable is interest receivable, which is the interest owed to the company by the entities to which it has lent money. The journal will not impact the expense, it simply reverses the interest payable and reduces cash balance.

Debits and Credits

So, you record the interest expense as a journal entry as soon as the loan is taken out, and not when you repay it at the end of the year or month. Before diving into some business examples on how to make journal entries for interest expenses, let’s first go over some accounting basics you’ll need to know. Long-term debts, on the other hand, such as loans for mortgage or promissory notes, are paid off for periods longer than a year. In this case, on April 30 adjusting entry, the company needs to account for interest expense that has incurred for 15 days.

Difference Between Interest Expense and Interest Payable

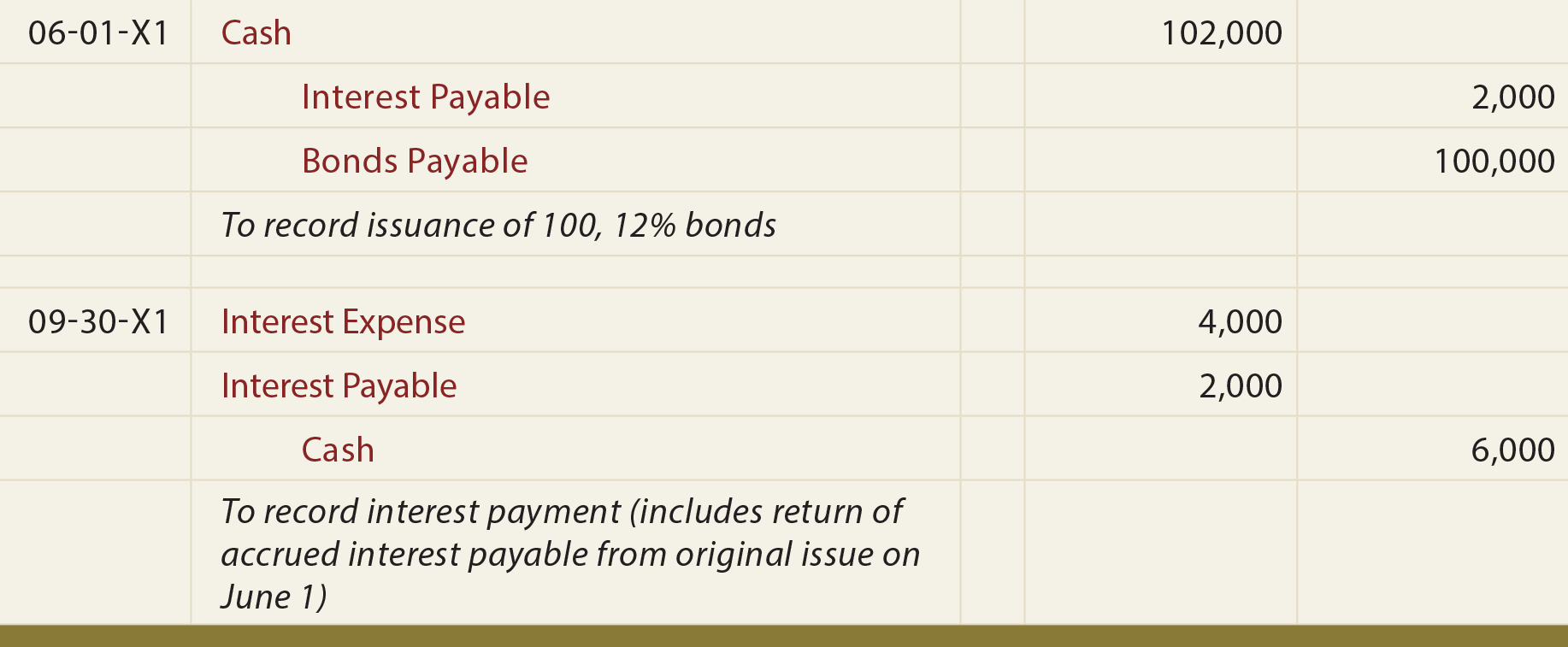

A note may be signed for an overdue invoice when the company needs to extend its payment, when the company borrows cash, or in exchange for an asset. Therefore, the November interest of $1,000 ($200,000 x 6% x 1/12) is to be paid on December 15. The $1,000 of interest incurred during December is to be paid on January 15. Therefore, as of December 31, the company’s current liability account Interest Payable must report $1,000 for December’s interest. For the two-month period, the company will report Interest Expense of $2,000 (November’s and December’s interest of $1,000 each month).

Journal Entries Playlist

- Interest expense is a type of expense that accumulates with the passage of time.

- Whether you are the lender or the borrower, you must record accrued interest in your books.

- Our mission is to provide entrepreneurs and small business owners with the knowledge and resources they need.

- If the company doesn’t record the above journal entry in the April 30 adjusting entry, both expenses and liabilities will be understated by $250.

You can also do this for entries based on estimates, so you can adjust for actual amounts at the end of the period. Short-term debts are paid within 6 months to a year and include lines of credit, installment loans, or invoice financing. For these types of debts, the interest rate is usually fixed at an average of 8-13%.

Any borrowing cost except those attributable to the acquisition, installation, or production of the qualifying asset is treated as the interest expense. In the case of equity financing, the money is owned by the company owners, who are shareholders. They are entitled to a profit in the company’s earnings up to the percentage of their investment. Understanding how to calculate interest expense is crucial for financial literacy and effective budgeting. In this detailed guide, we will delve into the intricacies of interest expense, providing a step-by-step walkthrough, expert insights, and answering common questions. Let’s demystify the process and empower you with the knowledge needed to manage your finances more effectively.

So, the recording of the interest expense will be on October 31st, for just one month of the year. This is helpful to business owners as it provides a clear overview of your cash flow, and that’s what potential investors will want to see, too. A low interest coverage ratio means that there’s a greater chance a business won’t be able to cover its debt.

A current liability account that reports the amounts owed to employees for hours worked but not yet paid as of the date of the balance sheet. As the company does the work, it will reduce the Unearned Revenues account balance and increase its Service Revenues account balance by the amount earned (work performed). A review of the balance in Unearned Revenues reveals that the company did indeed receive $1,300 from a customer earlier in December. However, during the month the company provided the customer with $800 of services. Therefore, at December 31 the amount of services due to the customer is $500.

Liabilities are traditionally recorded in the accounts payable sub-ledger at the time an invoice is vouched for payment. Both are liabilities that businesses incur during their normal course of operations but they are inherently different. Accrued expenses are liabilities that build up over time and are due to be paid. Accounts payable, on the other hand, are current liabilities that will be paid in the near future. In this article, we go into a bit more detail describing each type of balance sheet item. When a firm leases an asset from another company, the lease balance generates an interest expense that appears on the income statement.

The interest coverage ratio measures the ability of a business to pay back its interest expense. It’s important to calculate this rate before taking out a loan of any sort to make sure the business can afford to repay its debt. Then, find out how to set up the journal entry for borrowers and lenders and see examples for both.

Let’s say you are responsible for paying the $27.40 accrued interest from the previous example. Your journal entry would increase your Interest Expense account through a $27.40 debit and increase your Accrued Interest Payable account through a $27.40 credit. The company has already paid $3000 as interest expenses for September, October, and November. On the balance sheet, the company could only show “interest payable” of $1000 ($1000 for December).

Loans and lines of credit accrue interest, which is a percentage on the principal amount of the loan or line of credit. The interest is a “fee” applied so that the individual shared the lender can profit off extending the loan or credit. Also referred to as a “p.o.” A multi-copy form prepared by the company that is ordering goods.

More from my site

Americas strengthening dollar will rattle the rest of the world

Americas strengthening dollar will rattle the rest of the world MetaTrader 4 Trading Terminal from InstaForex: download MT4 for ..

MetaTrader 4 Trading Terminal from InstaForex: download MT4 for .. Аркада Live Casino 💰 Offers free spin 💰 400 Free Spins

Аркада Live Casino 💰 Offers free spin 💰 400 Free Spins โบนัสคาสิโนในพื้นที่โดยไม่ต้องฝากเงินเพื่อรับ Mobile People PlayStation World

โบนัสคาสิโนในพื้นที่โดยไม่ต้องฝากเงินเพื่อรับ Mobile People PlayStation World Mang trang phục gì khi đi biển Quan Lạn

Mang trang phục gì khi đi biển Quan Lạn Индикатор Zigzag Зигзаг в трейдинге: описание и применение статьи от Александра Герчика

Индикатор Zigzag Зигзаг в трейдинге: описание и применение статьи от Александра Герчика